Get your copy of Paul Forchione's book describing advanced techniques on futures options. Learn techniques from a professional options trader to manage risk while speculating on futures markets.

Click here to view Paul's eBook

By using our website, you agree to accept our terms of use (click to read)

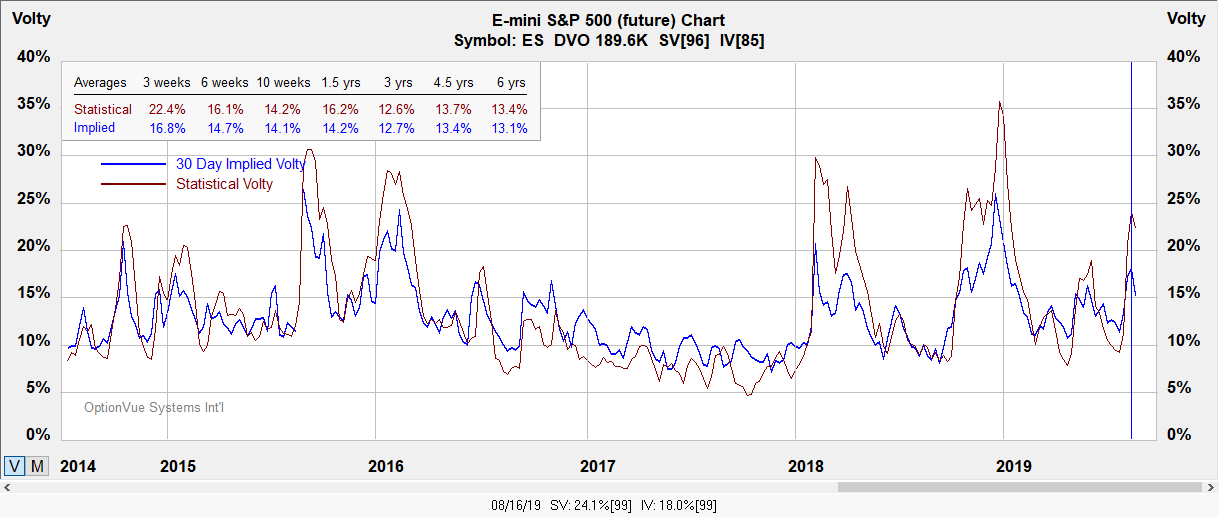

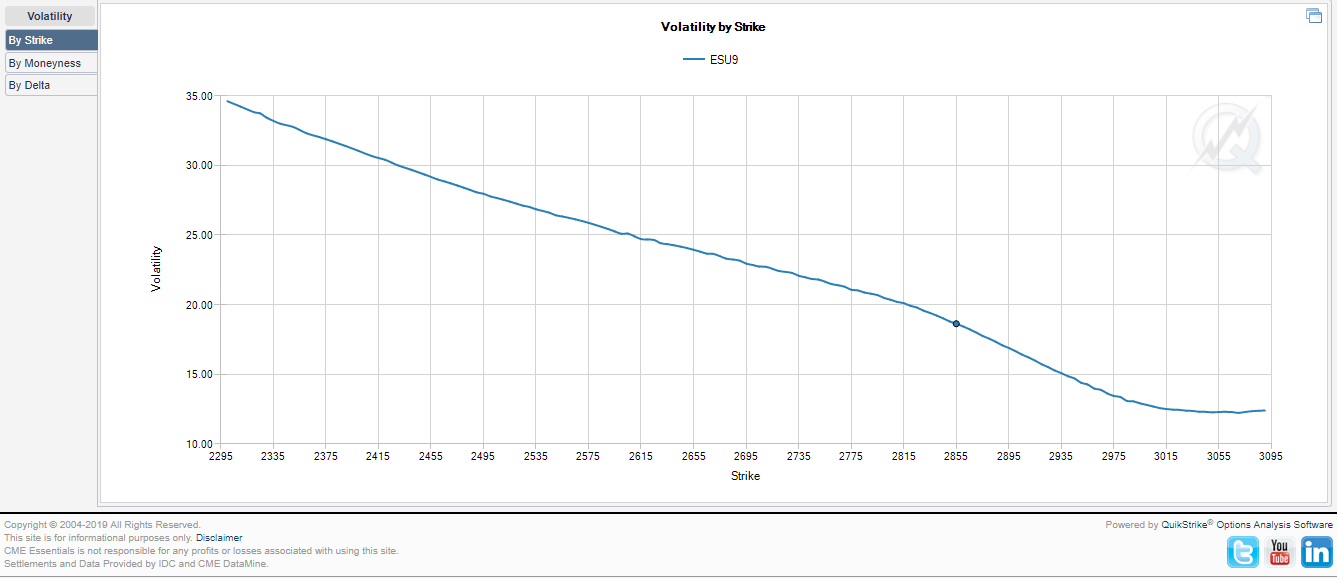

Volatility

Notes:

Contract Size - $50 x S&P 500 Index.

Tick Size: Outright: 0.25 index points=$12.50

Trading Hours: CME Globex: Sunday - Friday 6:00 p.m. - 5:00 p.m. Eastern Time (ET) with trading halt 4:15 p.m. - 4:30 p.m.

?ml=1" class="modal_link" data-modal-class-name="no_title">* Tip: Click here to read a helpful tip about E-Mini S&P futures and options

E-Mini S&P

Below are charts for reference.

?ml=1" class="modal_link" data-modal-class-name="no_title">* Tip: Click here on enlarging images

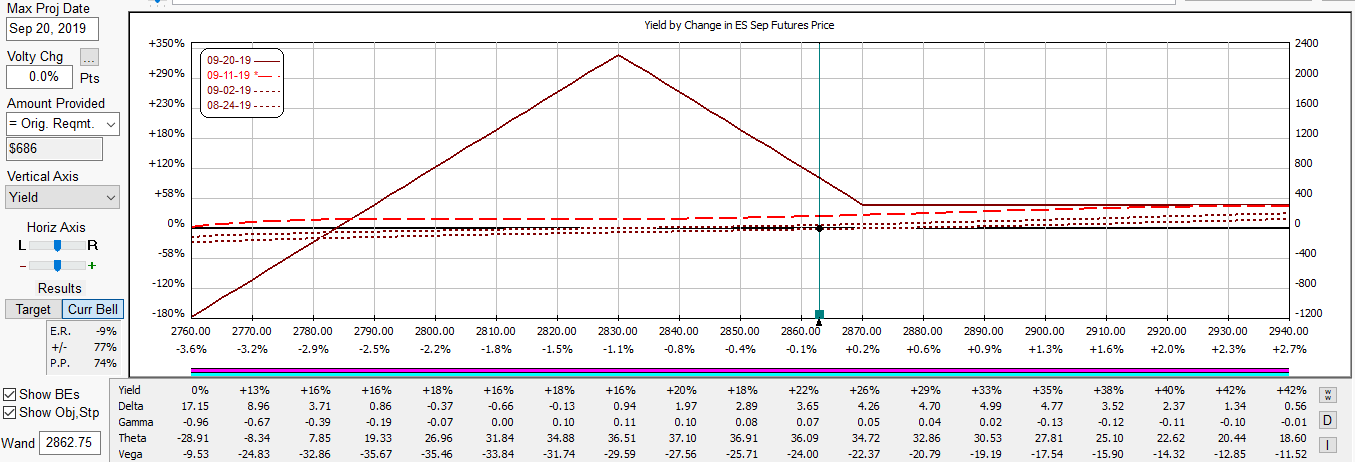

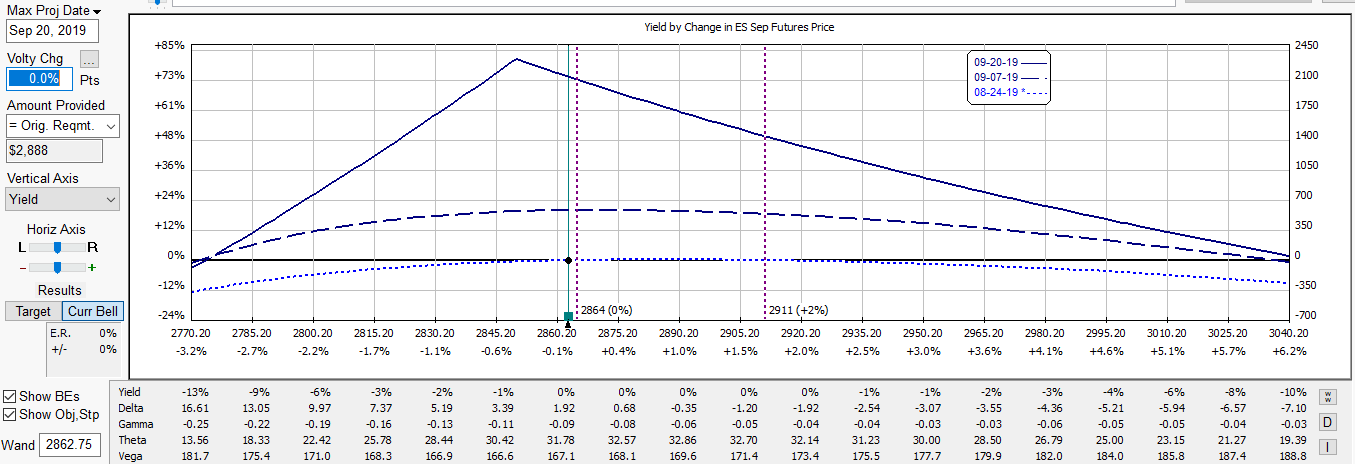

Strategies

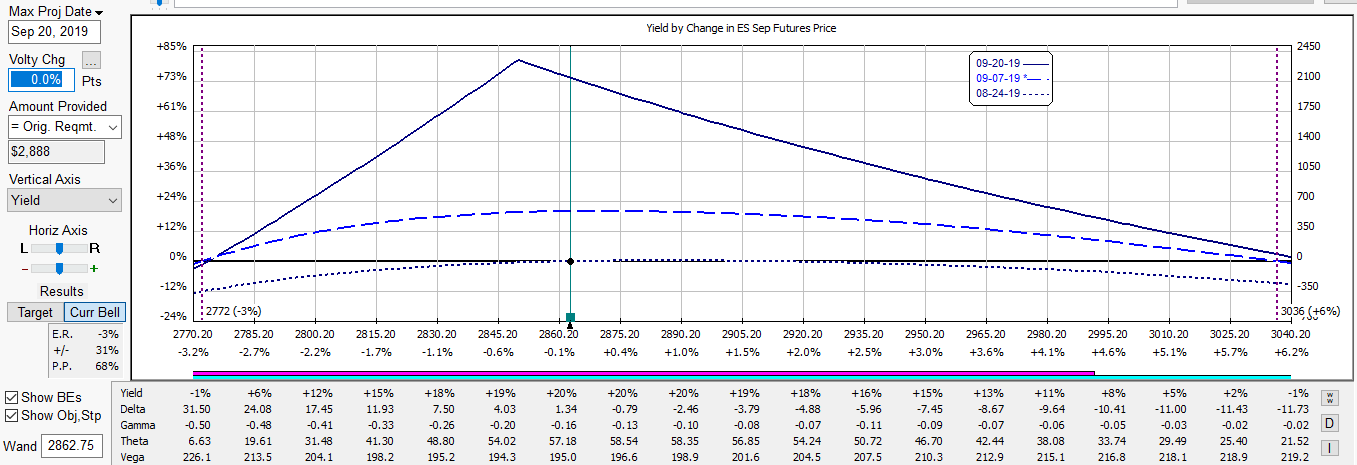

The % yield shown in the diagram below represent an estimated return on margin from projected dates shown.

Butterfly

The position below begins with a flat T+0 line covering a wide range of prices being delta neutral. It earns positive time decay and has negative Vega where if the market rebounds to the upside will earn an attractive return and benefit from a decline in implied volatility. If the market moved to extremes in the range, the position could be adjusted by layering additional spreads.

Calendar

The calendar spread below is delta neutral with positive Vega that would benefit the position if implied volatility rose from a sharp sell off. The illustration below starts with T+0.

The illustration below earns positive time decay as the position is held.

Join our Free Webcast each month and learn how these strategies can benefit your trading.