The following explanation and illustrations are an excerpt from CMEGroup’s publication, “Self-Study Guide to Hedging with Grain and Oilseed Futures and Options”. As an educational supplement, watch an example using a simple online hedge calculator in our newsletter. Take a quiz to help further your knowledge.

The Seller of Commodities

Commodity sellers, similar to commodity buyers, are potential hedgers because of their need to manage price risk. Commodity sellers are individuals or firms responsible for the eventual sale of the physical raw commodities (e.g., wheat, rice, corn) or derivatives of the raw commodities (e.g., soybean meal, flour). For example, commodity sellers can be farmers, grain elevators, grain cooperatives or exporters. Although they have different functions in the agricultural industry, they share a common risk – falling prices and a common need to manage that price risk. The following strategies for commodity sellers provide different risk management benefits.

Strategy #1: Selling Futures

Protection Against Falling prices

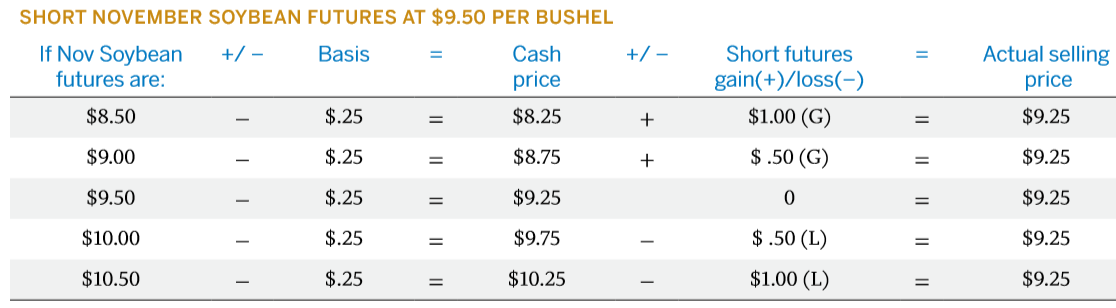

As a soybean producer, who just completed planting, you are concerned that prices will decline between spring and harvest. With Nov Soybean futures currently trading at $9.50 per bushel and your expected harvest basis of 25 cents under Nov Soybean futures, the market is at a profitable price level for your farm operation. To lock in this price level, you take a short position in Nov Soybean futures. Although you are protected should the prices move lower than $9.50, this strategy will not allow you to improve your selling price if the market moves higher.

A short futures position will increase in value to offset a lower cash selling price as the market declines and it will decrease in value to offset a higher cash selling price as the market rallies. Basically, a short future position locks in the same price level regardless of which direction the market moves.

The only factor that will alter the eventual selling price is a change in the basis. If the basis turns out to be stronger than the expected 25 cents under, then the effective selling price will be higher. For example, if the basis turns out to be 18 cents under November at the time you sell your soybeans, the effective selling price will be 7 cents better than expected. If the basis weakens to 31 cents under at the time of the cash soybean sale, then the effective selling price will be 6 cents lower than expected.

Action

In the spring, you sell Nov Soybean futures at $9.50 per bushel.

Expected selling price =

futures price +/– expected basis = $9.50 – .25 = $9.25/bushel

This email address is being protected from spambots. You need JavaScript enabled to view it.

Results

Assuming the Nov Soybean futures drop below $9.50 at harvest and the basis is 25 cents under, as expected, the lower price you receive for your cash soybeans would be offset by a gain in your short futures position. If Nov Soybean futures rally above $9.50 and the basis is 25 cents under, the higher selling price you receive for the soybeans will be offset by a loss on the short futures position.

Note the different price scenarios for the harvest time period (October) in the previous table. Regardless of the Nov Soybean futures moving higher or lower, the effective cash selling price will be $9.25 per bushel if the basis is 25 cents under. Any change in the basis will alter the effective selling price.

If the basis was stronger (20 cents under) when futures were at $8.50, the effective selling price would have been $9.30. If the basis weakened (30 cents under) when futures were at $10.50, the effective selling price would have been $9.20.

If you're a commodity risk manager looking for assistance on hedging, please visit our partner site OahuCapital.com for active assistance.